Investors are likely to think of the high-yield portion of the bond market as a small, specialized space reserved for only the very risk tolerant. While there certainly is elevated risk in loaning money to companies with not-so-stellar credit, junk bonds have become much more than a niche investment option. Current figures place the total value of domestic junk bonds somewhere between $1.5-2 trillion.

What Is A Junk Bond?

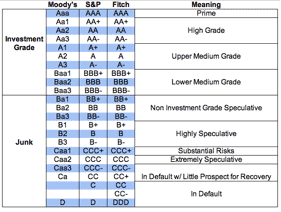

Technically speaking, a junk bond is a fixed-income security that has received a rating of Baa3 or less from Moody’s and/or BBB- from Standard & Poors, commonly referred to as S&P. Moody’s and S&P are the two main credit ratings agencies. Similar to stock analysts, the credit agencies analyze corporate balance sheets, cash flows, and business models in a attempt to ascertain relative ability to pay back obligations.

On a more general level, junk debt is any bond that is deemed to carry substantial risks. Of course when we look at the chart here, a bond rated BB+, while technically a junk bond, is only an upgrade away from being considered investment grade. On the flip side, a bond rated BBB- by S&P is only one step away from falling into the high-yield category.

Why Buy A Junk Bond?

Given the perception for a junk-rated company to run into financial difficulties and/or default on its debt, investors receive a higher rate of interest for taking on that risk. For instance if an investor is looking to buy a 10-year bond from an investment grade entity, it’s possible that they may receive only 2-4%, depending on the company’s debt that is selected. If, however, the same investor looks at junk-rated bonds with 10-year maturity, the reward jumps to a range of 4-7 percent.

So the main benefit to junk debt is the higher rate of interest that it offers. Of course this is no free lunch – high-yield issuers do default from time to time, which has varying consequences on an investment, none of which is generally positive.

And though the default rate continues to run at a multi-year low – Moody’s places it now below 2% – investors should not become complacent that that will continue infinitum. Indeed, if we look back to the financial crisis a little over five years past now, defaults spiked to the low double digits, which provided for a lot of sleepless nights for those that overweighted the space.

Strategy Session

If you’ve read this far, you still may think junk debt is right for a portion of your overall investment pie. But how much? Generally, I don’t think high-yield products, equity or fixed-income, should make up a large portion of a portfolio. Unless you are a seasoned credit analyst, are highly risk tolerant, or have reason to otherwise believe that junk bonds are a slam dunk, I think less than 10% allocation is in most cases prudent. For those that are risk intolerant, the allocation should even be lower, with perhaps a ceiling of 5 percent.

While I’m generally not a fan of bond funds, in the case of junk debt, I make an exception. Given the instant diversification and professional credit management that a fund affords, I think a high-yield fund is a solid, core idea for the average retail investor. There are many ETFs that track the junk market. For those looking for value, and/or a more aggressive way to play the space, there are leveraged closed-end funds trading at discounts to net asset value that can yield upwards of 10 percent.

Once you have a core position, then I think it may make sense to tippie-toe into individual issues. Still, I don’t think investors should get cute in high-yield land with a somewhat uncertain global and domestic macroeconomic situation still evolving. I would opine that things can turn on a dime in this environment, which would add fuel to being respectful, if not fearful, of junk risk.

Click here to learn more about best forex brokers.

About the author: Adam Aloisi has over two decades of experience investing in equities, bonds, and real estate. He has worked as an analyst/journalist with SageOnline Inc., Multex.com, and Reuters and has been a contributor to SeekingAlpha for better than two years. He resides in Pennsylvania with his wife and two children. In his free time you may find him discussing politics, playing golf, browsing antique shops, or traveling.

About the author: Adam Aloisi has over two decades of experience investing in equities, bonds, and real estate. He has worked as an analyst/journalist with SageOnline Inc., Multex.com, and Reuters and has been a contributor to SeekingAlpha for better than two years. He resides in Pennsylvania with his wife and two children. In his free time you may find him discussing politics, playing golf, browsing antique shops, or traveling.

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

Adam Aloisi