A recent article by Bloomberg, “Rigged Libor Hit States-Localities With $6 Billion” made it sound like Municipalities made bad financial bets.

A recent article by Bloomberg, “Rigged Libor Hit States-Localities With $6 Billion” made it sound like Municipalities made bad financial bets.

Municipalities bought around $500 billion of interest rate swaps prior to the beginning of the financial crisis, where they agreed to pay a fixed rate of interest in order to receive a market based interest rate. Interest rate swaps enable one to take a position on the direction of interest rates. The municipalities were taking the position that interest rates (specifically the 3-Month LIBOR rate) were going to rise over time. Instead, the 3-Month LIBOR rate fell, resulting in billions of dollars of losses for the municipalities.

What went wrong?

The big picture is that the bottom fell out of interest rates following the financial crisis, primarily due the the unprecedented market intervention of the Federal Reserve. As a result, the interest rate swaps turned out to be a money losing trade for the municipalities and many are trying to get out of the transaction.

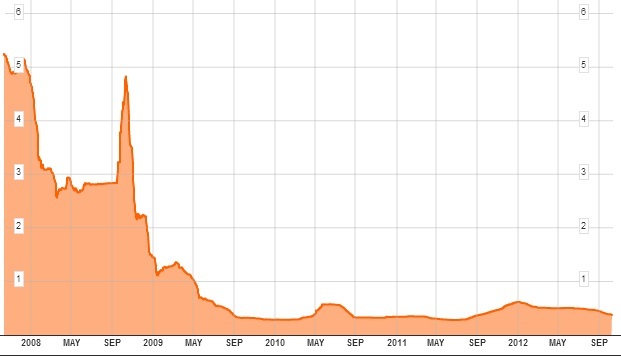

3 Month LIBOR Chart – 3 month LIBOR is currently 0.35%

Banks Were Also “Cheating” To Make The LIBOR Rate Low

At the same time that interest rates were dropping, banks were manipulating the 3-Month LIBOR rate for their own interests. Barclays Bank has agreed to pay $450 million in fines related to its manipulation of a variety of LIBOR rates. The 3-month LIBOR is supposed to measure the average rate which non-us banks make US dollar 3-month loans to each other. Instead of honestly reporting their borrowing cost, Barclays and others “reported” rates in way which may have suppressed the rate in the period before the financial crisis.

Should Municipalities Be Entering Into Interest Rate Swap Agreements?

This is the key question. Just because the municipalities lost money on the interest rate swap does not mean its a bad idea. There are two valid reasons that I can see for a municipality entering a interest rate swap.

A) To lock in a rate – Many municipalities issued floating rate bonds (such as Variable Rate Demand Notes). A municipality could turn their floating rate bonds into fixed rate debt, by using an interest rate swap. In other words, the municipality could gain certainty about their interest rate expenses. In this case, any money lost on the interest rate hedge would in fact be matched by lower interest rate expenses on the municipality’s debt.

B) To hedge rising rates for an upcoming bond issue – A municipality might have a new bond issue coming to market or might have bonds maturing that they need to re-finance. If the municipality’s finance team was worried about where interest rates might be in a 6 months or a year year, they might enter into a swap agreement. If interest rates moved higher, they might have to pay a higher interest rate on the bonds but would be receiving more money from the interest rate swap.

In both the above examples, the primary purpose of the interest rate swap was not to make profits. In the first case, the interest rate swap enables the municipality to turn a variable expense into a fixed one. In the second case, the municipality was trying protect against rising interest rate costs. These are both good reasons to buy interest rate swaps.

Slippery Slope Between Hedging And Gambling

There is an important difference between hedging out a specific risk and a generalized one. I believe a hedge is a transaction designed to eliminate or offset a defined risk. For example, a municipality has to re-finance a $10 Million bond issue in 2 years and is worried about interest rates rising during this time.

Almost all municipalities borrow money on a fairly regular basis. In some sense, an argument can be made that municipalities should always be thinking about ways to minimize the potential impact of increases in interest rates. However, this is the type of thinking that financial people use to justify trading. An interest rate swap which is taken on to offset general concerns about rising rates is gambling.

Learn More

- 5 Tips For Municipal Bond Investors from BlackRock’s Peter Hayes

- High Yield Municipal Bond Funds – What You Need to Know

- Should California’s $16 Billion Deficit Cause Municipal Bondholders to Run?

- How to tell if a Municipal Bond is Tax Free?

Click here to learn more about best forex brokers.

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account