Duke Energy is the largest electric power holding company in the United States, supplying roughly 7.7 million customers across an area of more than 100,000 square miles with either electricity or gas. The company’s electric customers can be found in North Carolina, Florida, Indiana, South Carolina, Ohio, and Kentucky, and gas customers are located in Ohio and Kentucky. Duke Energy also has international operations in Latin America and a 25% interest in a Saudi Arabian producer of MTBE called National Methanol Company.

Duke Energy is the largest electric power holding company in the United States, supplying roughly 7.7 million customers across an area of more than 100,000 square miles with either electricity or gas. The company’s electric customers can be found in North Carolina, Florida, Indiana, South Carolina, Ohio, and Kentucky, and gas customers are located in Ohio and Kentucky. Duke Energy also has international operations in Latin America and a 25% interest in a Saudi Arabian producer of MTBE called National Methanol Company.

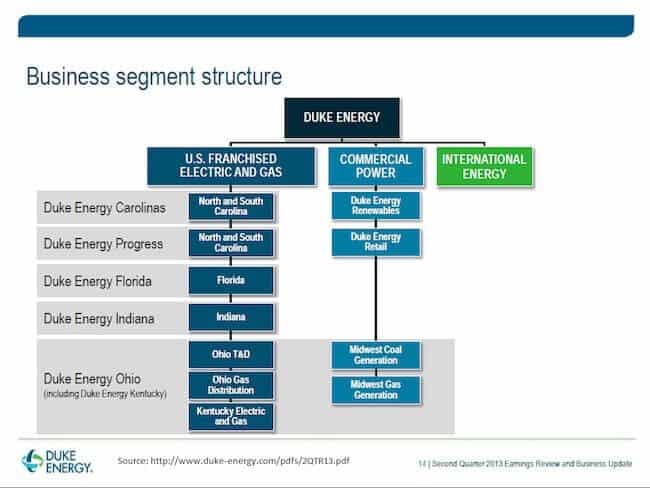

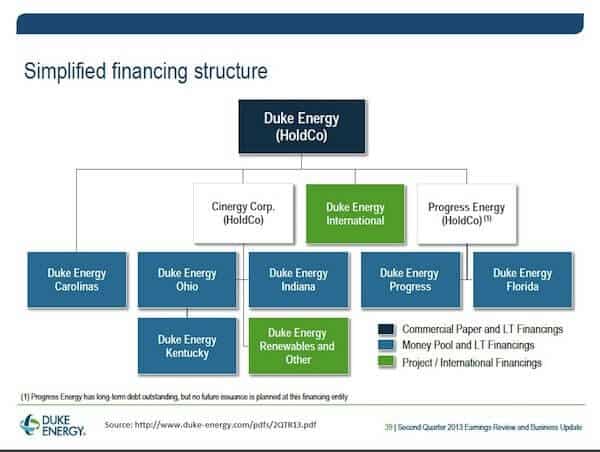

I realize there are all sorts of investors who have a variety of ways of approaching a potential new investment. When I search for investment opportunities, I first focus my efforts on the features of the security, and, if the security seems intriguing, I move on to a review of the business backing that security. For the purposes of this article, rather than simply presenting the features of the security hinted at in the title, I’d also like to make sure everyone is on the same page with respect to background knowledge of Duke Energy. Therefore, in addition to the information presented in the opening paragraph, I would also like to direct your attention to the following two slides from the company’s August 7, 2013, “Earnings Review and Business Update.” The slides outline the business and financing structures of Duke Energy.

Investing in the common stocks of utilities is certainly a popular way for income-focused investors to capture respectable yields. Concerning Duke Energy, my hunch is that utilities investors, in general, focus on the stock. Given the relatively unattractive yields on Duke’s senior unsecured debt, the lack of access for most investors to the senior secured debt of Duke’s subsidiaries, and the fact that there are currently no series of preferred stock outstanding, it is certainly understandable why investors might focus on the common stock. But in this case, the common stock, preferred stock, senior unsecured debt, and senior secured debt don’t make up the entire capital structure. And the missing piece might be of interest to some investors—especially those who like to invest in preferred stocks.

DUKH is the ticker symbol belonging to Duke Energy Corporation’s 5.125% Junior Subordinated debt. Rather than trading under its CUSIP (26441C303), this bond is exchange-traded and trades under the ticker DUKH. This exchange-traded debt security is a bit different from the bonds you are perhaps used to owning. While it is always a good idea to read through the prospectus prior to purchasing a bond, in this case, I would like to add particular emphasis to the fact that in addition to your due diligence on Duke Energy, you should read through the prospectus before purchasing DUKH. But before you spend your time digging through a prospectus for a security in which you may have no interest, let me share the highlights with you.

1. DUKH matures at $25 per share on January 15, 2073. Some investors may see a maturity date of 2073 and immediately turn their attention elsewhere. But let me remind readers that this security is a type of preferred-stock/bond hybrid. Many of the preferred stocks you will come across nowadays are perpetual preferreds, meaning they have no maturity date. By adding a maturity date, albeit one that is likely to occur after many of us have passed away, DUKH has a structural advantage over perpetual preferreds. After all, the price of this junior bond will one day, absent a default by Duke Energy, mature at $25. Perpetual preferreds have no such certainty regarding share price. Another structural advantage DUKH has over preferreds is that it is higher up the capital structure.

2. Two structural disadvantages to many (but not all) preferreds include DUKH’s distributions not qualifying for lower dividend tax rates and that DUKH does not have a redemption feature in the event of a takeover. In the event of a takeover, many preferred stocks (including non-convertible preferreds) allow for the conversion of the preferred into common stock. Bonds typically rectify this concern with “Change of Control” provisions, but DUKH does not include a put option for a change of control.

3. Interest is paid quarterly (similar to preferreds), as opposed to the semiannual interest payments that are so common among bonds.

4. There is a multifaceted call feature including a make whole call until January 15, 2018, a conditional call until January 15, 2018 for a tax event, a conditional call until January 15, 2018 for a rating agency event, and a continuous call at $25 per share on or after January 15, 2018.

5. Similar to many preferred stocks, DUKH can defer distributions. Deferred distributions can occur for up to 40 quarters, and, similar to how preferred stock distribution deferrals usually work, in the event DUKH defers distributions, Duke Energy would not be allowed to pay cash dividends on its common stock or any preferred stock outstanding during the deferral period. Furthermore, during a deferral period, Duke Energy would not be allowed to buy back stock or make any principal or interest payments on any debt securities equal or junior in right of payment to DUKH. Additionally, a deferral period may not extend beyond the maturity date.

6. One major difference between a deferral period for DUKH versus that of a preferred stock (whether a cumulative preferred or not) is that should Duke Energy defer interest payments, interest on the debentures will not only continue to accrue at 5.125%, but interest on the deferred interest will also accrue at 5.125%, compounded quarterly. Essentially, in the event of a distribution deferral, DUKH turns into a zero-coupon bond. Depending on what other income-paying securities are yielding at the time, investors might actually prefer to have deferred interest compound at a rate of 5.125% rather than being paid out. It should be noted that there are tax consequences associated with an interest deferral, and you should read the prospectus for further details.

7. On a final note, the 5.125% interest rate is 5.125% of $25 per share ($1.28125 per share per year). At the time this article was written, DUKH was trading well under $25 per share and yielding more than 6%.

If you are looking to build a diversified income stream that includes exposure to the utilities sector, DUKH is worth considering. In a future issue of the forthcoming LearnBonds newsletter (sign up here), I will further explore the topic of where on the capital structure income-focused investors might best be served.

Please keep in mind that this article is for informational purposes only and not a recommendation to buy or sell any securities. Only you can decide if taking the counterparty risk of investing in individual securities is right for you.

More from The Financial Lexicon:

Income Investing Insider Newsletter

The 5 Fundamentals of Building a Retirement Portfolio

Options Strategies Every Investor Should Know

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

The Financial Lexicon