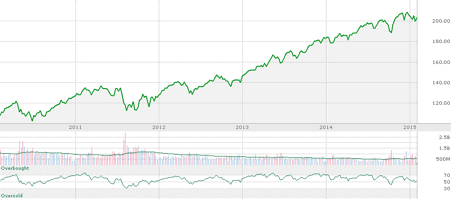

With the S&P 500 Index up 3-fold since lows hit at the height of the financial crisis in March of 2009, I don’t think I’m going out on a limb saying that stock investors probably won’t see that kind of return over the next six years. If collective equity returns revert to a more normal path of appreciation, an indexed large-cap portfolio may see only a fraction of that return. If the market decides to reprice lower, or wade water as it did between 2000 and 2010, a period sometimes now referred to as “The Lost Decade,” investors may end up being sorely disappointed over the next few years.

With the S&P 500 Index up 3-fold since lows hit at the height of the financial crisis in March of 2009, I don’t think I’m going out on a limb saying that stock investors probably won’t see that kind of return over the next six years. If collective equity returns revert to a more normal path of appreciation, an indexed large-cap portfolio may see only a fraction of that return. If the market decides to reprice lower, or wade water as it did between 2000 and 2010, a period sometimes now referred to as “The Lost Decade,” investors may end up being sorely disappointed over the next few years.

S&P 500 – 5 year chart

Stock seekers who wade outside the land of indexed equity into individual stocks typically start with a gravitation towards large-cap, household name dividend stocks. And with good reason. Companies like Procter & Gamble (NYSE:PG), Coke (NYSE:KO), Colgate (NYSE:CL), and Johnson & Johnson (NYSE:JNJ) possess large, global, established businesses, barriers to entry, as well as fairly predictable cash flows and forward dividend growth potential. Investors who own shares in these companies sleep well at night knowing that a destruction of operational fundamentals is unlikely.

But in this day and age of zero interest rate policy, affectionately known to some as “ZIRP,” there has been additional attraction to these kinds of stocks because they offer a dividend rate that is in excess of risk-free yields available. Risk-free investments usually include FDIC insured banking products as well as Treasury securities, although the latter, while are traditionally considered risk-free, really aren’t.

Again, this certainly isn’t madness, since equity returns have been been so robust. A move to stocks near the onset of this decade has paid off handsomely. However, there is a trade off as stocks appreciate in value. Stocks that may have been available at a low teens P/E (price to earnings) multiple six years ago, now may sell for upper teens multiples or even into the low twenties. If the growth rate of a company is not accelerating along with its valuation, which hasn’t happened to many of these dividend companies, the downside capital risk of investing in them — or even owning them — at these levels increases.

So although I don’t have a crystal ball, you should certainly not assume that this veritable straight line that we’ve been riding for the past many years continues on. In fact, odds are that your garden variety dividend companies may underperform on a total return level going forward — many of them already have been. The going may be especially bad if interest rates start to rise at a higher than expected clip. Why? Because those who gravitated to dividend stocks may start to lighten up on them in favor of higher yields available in risk-free investments, corporate bonds, or other fixed, rising payouts.

Still, I don’t think this admonition is necessarily cause for someone to churn their portfolio or avoid these kinds of stocks altogether. Conservative investors, retirees, dividend growth seekers, and those with otherwise risk intolerant profiles may continue to find solace in owning companies that aren’t going to disappear overnight. I do think this is a good time, however, to examine an overall portfolio allocation and critically analyze the need for richly valued dividend equity.

As one who currently ascribes to a value based investment philosophy, I think your better buys are companies that may be growing as fast as some of these dividend names, but are priced materially lower. I also think going outside the U.S. to corners of the globe that are again priced cheaper may be sound diversification at this juncture.

Buying global or small-to-mid-cap equities can be unnerving for someone who is used to the perceived safety of large-cap stocks. And admittedly it probably isn’t for everyone. However, I thinking dipping into pooled ETFs that invest in a basket of international stocks or focus on small-caps or other value situations may be a reasonable solution for a portion of one’s portfolio.

In the end, as I frequently preach to the individual investor, risk management and avoiding the “bad” security is just as important as searching for the one that becomes the next Microsoft, Apple, or Coke. As stock valuations rise, a good company may not necessarily make for a good investment at every point in time. Caveat emptor.

Adam Aloisi was long both Colgate and Johnson & Johnson at time of writing, but his positions may change at any time.

Disclaimer: The above should not be considered or construed as individualized or specific investment advice. Do your own research and consult a professional, if necessary, before making investment decisions.

About the author: Adam Aloisi has over two decades of experience investing in equities, bonds, and real estate. He has worked as an analyst/journalist with SageOnline Inc., Multex.com, and Reuters and has been a contributor to SeekingAlpha for better than two years. He resides in Pennsylvania with his wife and two children. In his free time you may find him discussing politics, playing golf, browsing antique shops, or traveling.

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

Adam Aloisi