With the first Fed move to tighten interest rates in almost a decade now behind us, economists as well as fixed-income investors are honing in on the prospects for additional hikes this year. While central bankers seem to be biased toward implementing a string of increases during 2016, I would opine that we all should be a bit suspect of that actually happening.

The 10-Year Treasury Yield

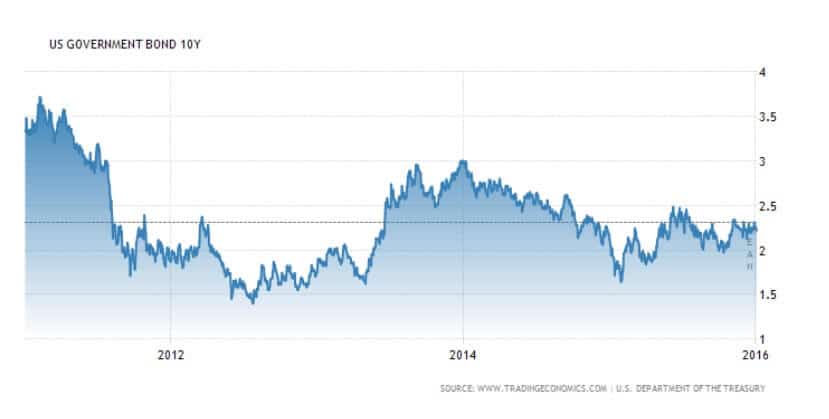

Over the past five years, the 10-Year Treasury yield, a commonly referred to investment grade rate measure, has traded mostly in a 1.5%-3% range. As you can see in the chart below, the mean (or average) rate (represented by the horizontal dotted black liine) has been about 2.3%, which is right about where the yield sits during this first week of January.

After a swift rate decline during the summer of 2011 due to Eurozone credit concerns, the so-called “taper tantrum” of 2013 doubled the 10-year yield heading into 2014. Despite concerns that an end to QE would signal a higher rate environment and potentially a 4% 10-year, rates, surprisingly to many, moved a full point in the opposite direction over the next 12 months.

As the reality of a weaker than expected macroeconomy became clear, rates spent the majority of 2015 in a low, tighter range than years past, mostly 2-2.4 percent.

Oil prices continued their downward spiral in 2015 and have heightened liquidity concerns amongst the more leveraged energy companies. Towards the end of the year the potential domino effect of such a scenario created a quasi-panic in the high-yield market, which seems to have stabilized. However, it brings to the surface just how jittery investors seem to be nowadays. And maybe with good reason.

What’s Happening to Rates Now?

Although Fed commentary and action would make one believe that we are on the cusp of some sort of meaningful expansion, the long end of the bond market doesn’t seem to share that contention. Long rates barely budged following last month’s Fed announcement and the 10-year still sits markedly lower than in did at the onset of 2014. Mixed data and conflicting opinion are leading some to believe that the yield curve will continue to flatten, and that ongoing Fed push to raise short-term rates could move us into recession. Read more about various yield curves and different economic scenarios.

As I’ve stated on a number of occasions over the past year, if we look at various data points relative to the housing market and middle-class America, there are signs of stability, but not much indication of a sustainable recovery. John Q. Public may still be living in a house in which they are underwater in their mortgage, or may not be fiscally strong enough to qualify for a mortgage at all.

If the yield curve continues to flatten, it would create less incentive for lenders to go out on a limb for borrowers with marginal credit. Since bank lending operations rely on a strong spread between short rates and long rates to profit, a flat curve would not be a positive occurrence for the housing market, the average borrower, and consequently, the economy as a whole.

Where Are Rates Headed?

While the Fed may take another stab at a hike, my feeling is rather doubtful that we’ll see more than another 25 basis point move this year. A rickety first day of trading in global equity markets continues to signal widespread nervousness, both valuation- and growth-related, especially in emerging markets. The strong dollar will also be a continued hurdle to multinational conglomerates or consumer products companies with strong or even majority-revenue presence in countries outside the United States.

We can all be hopeful that we are entering a period of unfettered growth. However, there is much reason to believe that this is a “slippery slope of hope.” Although I’d opine that the economy is holding its own, it the Fed taps the brakes a bit too many times, I wouldn’t be surprised if it ultimately sends us backwards.

As it relates to the bond market, while the long end doesn’t seem to be very rewarding, if the economy sits in neutral or otherwise spin its wheels, it may continue to be the place to be. Still, the potential risks are rather high for going too far out on that limb, so I’d more inclined to focus in on intermediate paper with above average credit, which seems to be the continuing sweet spot for yield seekers in today’s bond market.

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

Adam Aloisi