A steady surge in the volume of reverse repo operations performed by the Federal Reserve is highlighting the risks of the ultra-accommodative policy adopted by the US central bank, as financial institutions in the country struggle to find places to park their excess reserves.

The decision adopted by the Federal Reserve to purchase as much as $120 billion per month in US Treasury bonds and mortgage-backed securities (MBS) to contain the financial fallout caused by the pandemic has flooded the country’s financial system with cash and that liquidity has been flowing down the drain until it has reached banks in the form of higher deposits.

These higher reserves, combined with weak demand for loans, have resulted in the accumulation of vast excess reserves, with financial institutions mostly allocating that money into fixed-income securities including Treasury bonds.

Even though the measure has been effective in containing the worst-case-scenario for the bond market, it appears to be backfiring now since banks are struggling to park their excess cash as they become increasingly worried about the risks of holding vast amounts of long-term bonds in their balance sheets, especially at a moment when inflation appears to be accelerating.

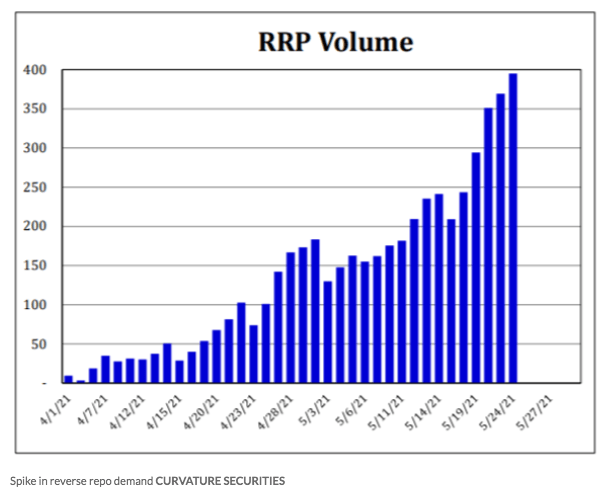

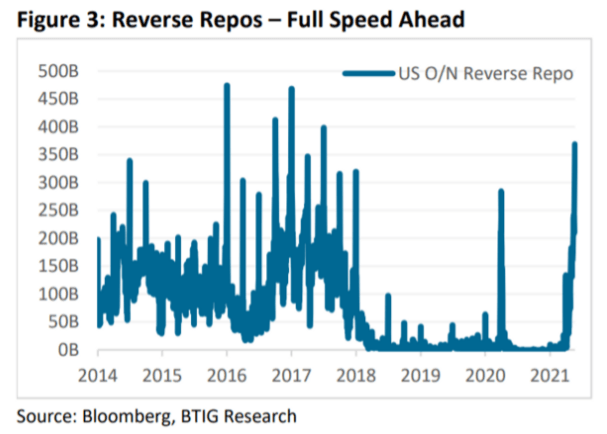

These concerns are reflected by the latest steady climb in the volume of reverse repo operations performed by the Federal Reserve Bank of New York – the branch of the US central bank in charge of conducting these transactions – as data shows that the institution performed an awfully odd $394.94 billion reverse repo operation on 25 May – the largest single-day transaction reported by the branch since the late 2017s.

A reverse repurchase agreement – also known as a reverse repo – is an operation in which Bank A agrees to receive cash from Bank B, with bank A pledging US Treasury securities as collateral for the transaction. Bank B is entitled to receive an interest for such loan at a rate commonly known as the overnight rate.

For now, the Fed has been able to maintain the overnight rate in positive territory by actively intervening in the repo market. They have achieved this by acting as the institution that receives the cash while paying the other party a minimum interest rate going from 0% to 0.1%.

However, as excess reserves continue to build up, the risk that the Fed may not be able to fully satisfy the market’s appetite for parking their reserves somewhere else could plunge repo rates to negative territory. This means that banks would start to pay other institutions to hold their cash.

If the situation comes to that, the big risk at the moment is that the Federal Reserve might be forced to raise rates much sooner than the market expects as a way to prevent repo rates from turning negative.

“Right now, the more money you put in, you get it right back”, said Scott Skyrm, executive vice president in fixed income and repo at Curvature Securities during an interview with MarketWatch.

He added: “The market is saying ‘It’s time.’ There is the evidence that QE has gone too far”, referring to the possibility that high demand for reverse repo operations from banks is signaling that the accommodative policy adopted by the US central bank has reached a tipping point.

How could this affect the financial markets?

The next meeting of the Federal Open Market Committee (FOMC) is scheduled to take place in mid-June and chances are that this could be an important topic of discussion.

Meanwhile, analysts who are viewing this situation in the reverse repo market as an indication that a shift in policy is due believe that the Fed could start to contemplate the idea of tapering its bond purchases in the short term.

Such a decision could cause some temporary volatility in the financial markets as it would signal a turning point in the accommodative policies that have so far supported stretched valuations in most asset classes.

Trusted & Regulated Stock & CFD Brokers

What we like

- 0% Fees on Stocks

- 5000+ Stocks, ETFs and other Markets

- Accepts Paypal Deposits

Min Deposit

$200

Charge per Trade

Zero Commission on real stocks

64 traders signed up today

Visit Now67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Available Assets

- Total Number of Stocks & Shares5000+

- US Stocks

- German Stocks

- UK Stocks

- European

- ETF Stocks

- IPO

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 Zero Commission

- NASDAQ Zero Commission

- DAX Zero Commission

- Facebook Zero Commission

- Alphabet Zero Commission

- Tesla Zero Commission

- Apple Zero Commission

- Microsoft Zero Commission

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

- Paypall

- Skrill

- Neteller

What we like

- Sign up today and get $5 free

- Fractals Available

- Paypal Available

Min Deposit

$0

Charge per Trade

$1 to $9 PCM

Visit Now

Investing in financial markets carries risk, you have the potential to lose your total investment.

Available Assets

- Total Number of Shares999

- US Stocks

- German Stocks

- UK Stocks

- European Stocks

- EFTs

- IPOs

- Funds

- Bonds

- Options

- Futures

- CFDs

- Crypto

Charge per Trade

- FTSE 100 $1 - $9 per month

- NASDAQ $1 - $9 per month

- DAX $1 - $9 per month

- Facebook $1 - $9 per month

- Alphabet $1 - $9 per month

- Telsa $1 - $9 per month

- Apple $1 - $9 per month

- Microsoft $1 - $9 per month

Deposit Method

- Wire Transfer

- Credit Cards

- Bank Account

Alejandro Arrieche