Everyday Loans Review 2021 – Do We Recommend it?

Are you in the hunt for a personal loan provider that is happy to consider applicants with bad credit? If so, it might be worth considering the merits of Everyday Loans. The lender facilitates loans of between £1,000 and £15,000, with repayment terms starting at 24 months, up to a maximum of 60 months.

Although the lender is somewhat flexible in who it offers financing to, it’s likely that you’ll pay a high rate of interest. In fact, the platform lists a representative rate of 93.6% APR, which is not only expensive, but it resembles that of a payday loan (Find out more about the best payday loans here).

With that being said, if you’re thinking about using the lender for your personal loan needs, we would recommend reading our Everyday Loans Review first. Within it, we cover everything from eligibility, APRs, loan terms, late payment fees, and more.

-

-

Try Our Recommended UK Payday Loan Provider 2020:

- Get an Instant Quote

- Apply within 2 Minutes

- Friendly Support Service

- FCA Regulated

*Subject to lender requirements and approval.When UK-based lenders advertise a ‘representative rate’, this is the rate that it chooses to market. As such, you could pay a higher rate than this, or, if your credit is good, less.What is Everyday Loans?

Everyday Loans is an online loan provider that specializes in personal loans. Launched in 2006, the platform allows you to complete the initial application process via your desktop or mobile device. With that said, as Everyday Loans also has a number of branches scattered throughout the UK, you will need to finalize the application process in person. Nevertheless, the platform is able to facilitate personal loans of between £1,000 and £15,000.

Although Everyday Loans does not market itself as a bad credit lender per-say, this is highly evident in the interest rates that it charges. For example, at a representative rate of 93.6%, this is an obscene amount of money to be paying on a long-term loan. On the contrary, high-street banks offer similar loan packages at interest rates of sub-5%. However, this is on the proviso that the borrower has a good or excellent credit score.

As a result, if you’re looking for a personal loan but your credit rating is less than ideal, you might be forced to use a lender like Everyday Loans. The platform allows you to borrow the funds at a minimum term of 2 years, up to a maximum of 5 years. The interest that you pay will always remain fixed throughout the term of the loan, as will your monthly repayments.

All of the loans offered by Everyday Loans are unsecured, meaning that there is no requirement to be a homeowner. Moreover, the lender does not charge any application fees, nor will you be charged an origination fee. Instead, everything is built into the underlying APR. Finally – and perhaps most importantly, Everyday Loans utilizes a soft credit inquiry when you first apply. As such, you’ve got nothing to lose by finding out your personalized interest rate.

What are the Pros and Cons of Everyday Loans?

Everyday Loans Pros:

✅Transparent on fees

✅Suitable for those with a less than ideal credit score

✅Personal loans of between £1,000 and £15,000

✅Loan terms of between 24 months and 60 months

✅Utilizes a soft credit inquiry when you first apply

Everyday Loans Cons:

❌ A representative rate of 93.6% is super-high

❌ Required to finalize loan application in-branch

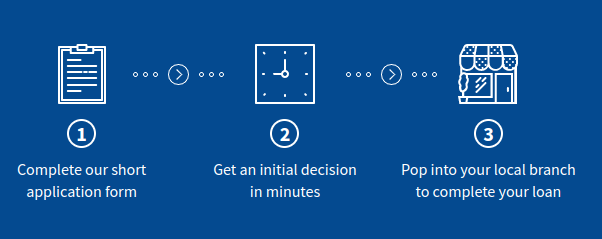

How Does Everyday Loans Work?

In a similar nature to fellow personal loan counterparts Satsuma Loans and Cash Float Loans, Everyday Loans allows you to initiate the loan process online. As such, you’ll need to head over to the Everyday Loans homepage to get the ball rolling. Once you click on the ‘APPLY NOW’ button, you’ll be asked to enter a range of personal information.

This will include your full name, address, date of birth, and national insurance number. You’ll also need to stipulate your employment status, take-home salary, and the frequency in which you get paid. Once you have provided the required information, you’ll get to choose how much you wish to borrow (£1,000-£15,000) and for how long (24-60 months).

The most important thing is that the initial application at Everyday Loans will not be posted to your credit report. As such, you’ve got nothing to lose by finding out what rates are available. If you deem the rates too high, simply walk away.Once you submit the application form, the Everyday Loans system should give you a decision in less than 30 seconds. If the lender deems you suitable for financing, you’ll be presented with your loan terms. This will include the amount it is happy to lend you, and the underlying interest rate. At this stage of the application, you are under no obligation to proceed.

If you are happy with the financing terms offered by Everyday Loans, you will need to visit your nearest branch to finalize the agreement. This is a major pain-point, as most lenders in the space allow you to complete everything online. Nevertheless, once you’ve signed the physical loan agreement, you should receive your loan funds within 1 working day.

Will Everyday Loans ask for Documents?

You will need to bring a number of documents with you when you visit your local Everyday Loans branch. These need to be original copies.

✔️ Valid ID

Everyday Loans requires you to bring one form of ID with you. This will need to be a passport or driver’s license. If you’re self-employed and working in the construction industry, you’ll also need to provide a photographic registration card (for example – form C1S4).

✔️ Proof of Address

You’ll also need to bring a document that verifies your home address. This can include a recent utility bill or bank statement. Everyday Loans will also accept a television license renewal letter, or a car tax statement from the DVLA.

✔️ Proof of Earnings

You will need to bring a copy of your recent payslip. This needs to be dated within the last 60 days. If you’re self-employed or running a business, Everyday Loans will accept the previous year’s audited accounts, or a self-assessment return.

✔️ Regular Outgoings

In order to determine whether or not you are able to afford a personal loan, you will need to show the lender what regular outgoings you have. This includes metrics like your rent or mortgage payments, phone bill, or utility payments. As such, Everyday Loans will need to see bank statements for the last two months.

What Types of Loans Does Everyday Loans Offer?

Although Everyday Loans specializes in personal loans, it does offer financing for specific purposes. This includes:

✔️ Personal Loans

✔️ Bad Credit Loans

✔️ Debt Consolidation Loans

✔️ Car Loans

✔️ Wedding Loans

✔️ Loans for Couples

✔️ Loans for Young People

✔️ Guarantor Loans

How Much Does Everyday Loans Cost?

As we noted earlier in our review, Everyday Loans offers a representative rate of 93.6% APR. However – and as is the case with all representative rates, this is merely the APR that the lender wishes to advertise. As such, the specific interest rate that you are offered will depend on a number of variables. Moreover, you won’t know what the rate is until you complete the initial application.

Nevertheless, Everyday Loans will base your interest rate on the following factors.

❓The amount you need to borrow

❓How long you need to borrow the funds for

❓Your current credit score

❓How much you earn

❓Your debt-to-income ratio

❓Your regular outgoings

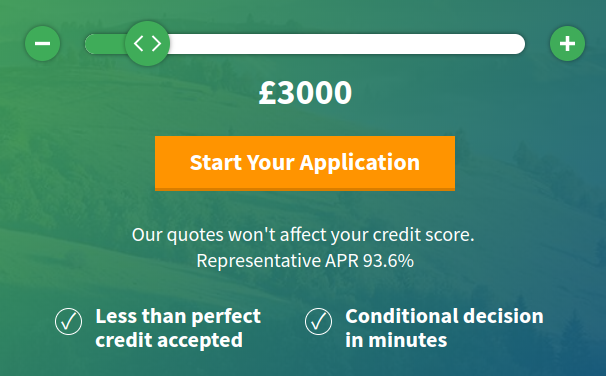

Although Everyday Loans allows you to make the initial application via a soft credit inquiry, if you proceed with the terms offered the lender will then need to run a hard credit check.💸 In terms of assessing how much a loan will cost you in pounds and pence, it’s probably best that we give you an example using the lender’s representative rate of 93.6% APR. Let’s say that you were to borrow £3,000 over the course of 2 years. You would be required to make 24 fixed monthly payments at £231.78.

💸 This means that the £3,000 loan will cost you £2,562.75 in interest, amounting to an overall total of £5,562.75. This is an incredible amount of interest to be paying, which is why Everyday Loans should be a last resort.

💸 With that being said, Everyday Loans does offer a top-rate APR of 30.5%, which is much lower than the representative rate it offers. However, in comparison to high-street lenders, this is still a lot of interest to be paying on a personal loan. At the other end of the spectrum, the maximum rate that you could pay at Everyday Loans is 249.5% APR.

💸 Finally, Everyday Loans does not charge any application or origination fees, which is a bonus.

Am I Eligible for Financing With Everyday Loans?

As is to be expected with a lender that charges super-high APR rates, Everyday Loans is very flexible with who it lends money to. This is why the lender asks you to bring in multiple supporting documents, as it doesn’t base its decision primarily on your credit score.

Make sure that the information you enter during the application process is 100% correct, as you will need to verify this in person before the loan is finalized.However, not everyone will be eligible to borrow funds from the lender, so we’ve listed the main criteria that you’ll need to meet below.

✔️ Full-Time Employment

One of the main metrics that Everyday Loans will look at is whether or not you are employed full-time. If you aren’t, your application is likely to be rejected.

✔️ Income

On top of being employed full-time, Everyday Loans will look at how much you earn after tax. The lender does not state what the minimum earning threshold is, so this will be judged against metrics of your overall financial standing.

✔️ Age and Residency

You need to be aged at least 18 years old and be a UK resident.

✔️ Affordability

Everyday Loans needs to make sure that you are able to afford the personal loan you wish to take out. They will do this by looking at what regular outgoings you have throughout the month.

✔️ Current Debt Levels

The lender will also need to assess what debt obligations you currently have. As such, if you’ve got heaps of credit cards and loan agreements that are still outstanding, you might not qualify with Everyday Loans.

Customer Service at Everyday Loans

If you need to speak with a member of the Everyday Loans customer service team, you can either call your local branch or send an email. You’ll find the respective telephone number via the lender’s website upon entering your postcode. Emails need to be sent via the online contact form.

📱Phone: Call Your Nearest Branch

📧 Email: Online Contact Form

✉️ In Writing: Everyday Lending Limited, Secure Trust House, Boston Drive, Bourne End, Bucks SL8 5YS

Everyday Loans Review: The Verdict?

In summary, Everyday Loans certainly has its good points. The lender allows you to borrow between £1,000 and £15,000, with loan terms starting at 24 months, up to a maximum of 60 months. Moreover, not only is the initial application super-easy, but it’s based on a soft credit inquiry. As such, finding out your personal loan terms is virtually risk-free. However, Everyday Loans also comes with its flaws.

At the forefront of this is the APR rates that the lender charges. Based on its representative rate of 93.6% APR, a £3,000 loan over the course of 2 years would end up costing you £2,562.75 in interest. This is hugely expensive, and there are certainly cheaper lenders out there. With that being said, if you’re currently in receipt of a bad credit rating, you might be left with little choice but to use a high-APR lender like Everyday Loans.

Try Our Recommended UK Payday Loan Provider 2020:

- Get an Instant Quote

- Apply within 2 Minutes

- Friendly Support Service

- FCA Regulated

*Subject to lender requirements and approval.FAQ:

What is the lowest APR rate that I can get with Everyday Loans?

Although the representative rate promoted by Everyday Loans stands at 93.6% APR, it does faciliate loans from 30.5% APR. However, this is still somewhat expensive.

How much can I borrow from Everyday Loans?

Everyday Loans allows you to borrow a minimum of £1,000, upto a maximum of £15,000. Even if you are approved for a loan with lender, you might be offered less than what you applied for.

How will I receive my loan funds from Everyday Loans?

You will have your loan funds transferred to your UK bank account once the application has been finalized. However, you’ll first need to visit your nearest Everyday Loans branch to hand in a range of documents, and then sign the loan agreement.

Does Everyday Loans charge any origination fees?

Although most personal loan providers active in the UK lending space charge origination fees, Everyday Loans doesn’t.

UK Payday Loan Reviews- A-Z Directory

Kane Pepi

Kane Pepi

View all posts by Kane PepiKane holds academic qualifications in the finance and financial investigation fields. With a passion for all-things finance, he currently writes for a number of online publications.

Latest News

Halifax Share Dealing Review

If you’re looking for a low-cost share dealing platform that makes it super easy to buy and sell stocks, ETFs, and funds, it might be worth considering Halifax. You don’t need to have a current account with the provider, and getting started takes just minutes. In this article, we review the ins and outs of...

UK Banks Approved Nearly 1 Million Mortgages in 2019, 7.4% More than a Year Ago

The United Kingdom’s high street banks approved close to a million mortgages in 2019. Data gathered by LearnBonds.com indicates that 982,286 mortgages were approved in 2019, an increase of 7.4% from 2018’s 909,597. The mortgage approval entails loans for home purchase, remortgaging and other loans. Compared to 2018, the number of mortgages approved for home...

WARNING: The content on this site should not be considered investment advice and we are not authorised to provide investment advice. Nothing on this website is an endorsement or recommendation of a particular trading strategy or investment decision. The information on this website is general in nature, so you must consider the information in light of your objectives, financial situation and needs. Investing is speculative. When investing your capital is at risk. This site is not intended for use in jurisdictions in which the trading or investments described are prohibited and should only be used by such persons and in such ways as are legally permitted. Your investment may not qualify for investor protection in your country or state of residence, so please conduct your own due diligence or obtain advice where necessary. Crypto promotions on this site do not comply with the UK Financial Promotions Regime and is not intended for UK consumers. This website is free for you to use but we may receive a commission from the companies we feature on this site.

Copyright © 2022 | Learnbonds.com

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Scroll Up