10 Top Low-Interest Credit Cards For 2020 Compared

Credit cards offer convenient ways to make advance purchases to be paid on a later date. However, if your balance grows too big, the interest you pay on your card can significantly hurt your finances. There are various aspects to consider when choosing a credit card. Nevertheless, interest rates and annual APRs remain the most crucial part, especially if you plan to transfer balances to subsequent months.

Some credit cards charge shallow interests on the amount you borrow. Others even offer a zero-percent limited introductory rate. This means you do not have to pay any interest for a specified period, usually 12 -14 months. Unsurprisingly, APRs tend to shoot quite high following a long period of zero interest. There are also various other aspects to review when determining the best credit credit card for your unique needs. Here is a review of the top 10 low-interest credit cards in the US, including brief insights to help you understand your options.

Why should you consider low-interest credit cards?

I. Save you money on interest

As the name suggests, low-interest credit cards charge a very low annual APR compared to conventional credit cards. Most lenders also allow you to transfer bank balances at reasonably low rates. These offers are ideal if you have large balances or if your current card charges a high rate. Low-interest credit cards also come with lengthy introductory periods where you are not charged any interest on your purchases or bank transfers.

II. Makes it easy to manage your balances

If you often carry your balances into the next month, then you should give low-interest credit cards some thought. It significantly lowers the total interest you will pay and also makes it easier to calculate and manage your more significant credit balances.

III. To improve your credit score

By managing your balances, low-interest credit cards make it easier to pay your monthly installments on time. Your bank records these transactions and sends them to credit bureaus. You can, therefore, use them to build your score with each on-time payment you make.

Pros

- Saves you more on interests

- Ideal for large balances and merchant purchases

- Allows you to transfer balances

- Low minimum pre-qualification requirements

Cons

- High APRs on card transfers

- Added charges and late fees

Criteria used to rank the best low-interest credit cards

- Minimum eligibility requirements

- Introductory rate and period

- Annual APRs

- Availability of 0% interest

- Rewards and cashback programs

- Balance and credit card transfers

Top 10 low-interest credit cards

Citi Simplicity Credit Card is by far the best low-interest credit card in the market. They offer an extended 21 month 0% introductory APR on balance transfers and 12 months for purchases. Citi also charges no penalty fees or late APR. You are required to complete balance transfers within four months of opening an account. It is ideal if you want to transfer high-interest balances from other credit cards. After the introductory period, normal APRs range between 16.99% and 26.99% depending on your score and creditworthiness. Other features include a 5% charge on bank transfers, 3% on foreign transactions, and a $0 liability is unauthorized persons use your card.

Pros:

- No penalty fees or late APR

- You can choose your repayment due date

- $0 annual fees

- Low annual percentage rate

Cons:

- No cash backs, points or miles

- Bank transfers must be completed within four months

In addition to offering low APRs of only 14.24% – 25.24%, Discover it credit card comes with a reward program that allows you to earn 5% of your purchases back. The 5% reward rate is offered quarterly in different places, including select grocery stores, gas stations, restaurants, and Amazon.com. You also earn 1% unlimited cashback on all purchases made. Discover it charges no annual fees and offers a 14 month 0% introductory APR on bank transfers. You can also subscribe to their free notification service that informs you if your social security number is found in any dark web platform.

Pros:

- Allows you to earn back cash

- Non-expiring redeemable rewards – any amount at any time

- Low APRs on balance transfers

- Extended 14-month zero-interest APR

Cons:

- The zero-interest period only applies to balance transfers

- Variable APR

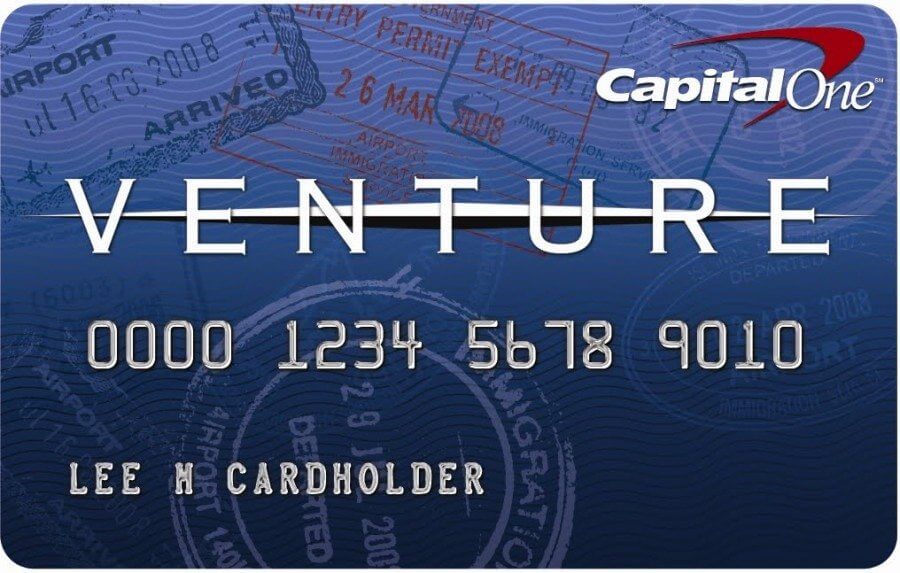

Venture One credit card by Capital One is another low-interest card you can apply for especially if you like to travel. The card uses a reward system that allows you to earn miles on the amount you spend on your card. You can earn up to 20,000 miles if you spend a minimum of $1,000 within the first three months of opening your account. This is the equivalent of $200 in air travel. You also earn 1.25X miles on every purchase you make and 10X miles on hotels. Venture one has a 0% 12-month introductory APR on purchases and variable APRs between 14.24% and 24.24%.

Pros:

- Charges $0 annual fees

- Travel with any airline and stay in any hotel with no blackouts

- Miles never expire

- No balance transfer APR

Cons:

- The zero-interest APR does not apply to bank transfers

- Variable APRs

HSBC Gold MasterCard offers customers an affordable low-interest card idea for financing major purchases. While this offer is slightly different from other credit cards in the list, it has similar features. The card offers an 18-month 0% introductory APR on both balance transfers and purchases. HSBC charges low-interest APRs of 13.24% – 17.24% for customers that have an above-average credit score. No annual fees and foreign transaction fees are required. You can also get a cash advance with an APR of 27.24%.

Pros:

- Significantly reduced interest rates

- No annual fees and foreign transaction fees

- Extended 18-month zero-interest period

- One year waiver on late payment

Cons:

- No sign-up bonus

- High eligibility requirements

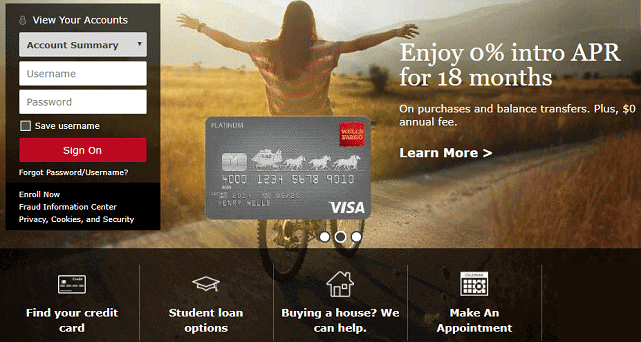

Wells Fargo Platinum credit card has an extended opening period of 18 months on both purchases and bank transfers. Following this duration, normal APRs range from 13.74% – 27.24%. You also get cash advance at 5% and 3% on balance transfers completed within the first 120 days of opening your account. No annual fees are charged, but you will be charged a late payment fee of $37. Other benefits include exceptional customer service and a resourceful inquiry section. Wells Fargo also offers free tools for digital budgeting and calculations.

Pros:

- Low cash advance rate for transfers within 120 days

- Cell phone protection reimbursement of up to $600

- Low APRs and extended introductory purchase 0% APR

- Zero liability on unauthorized transactions

Cons:

- Charges late and returned payment fees

- Requires good to excellent credit score

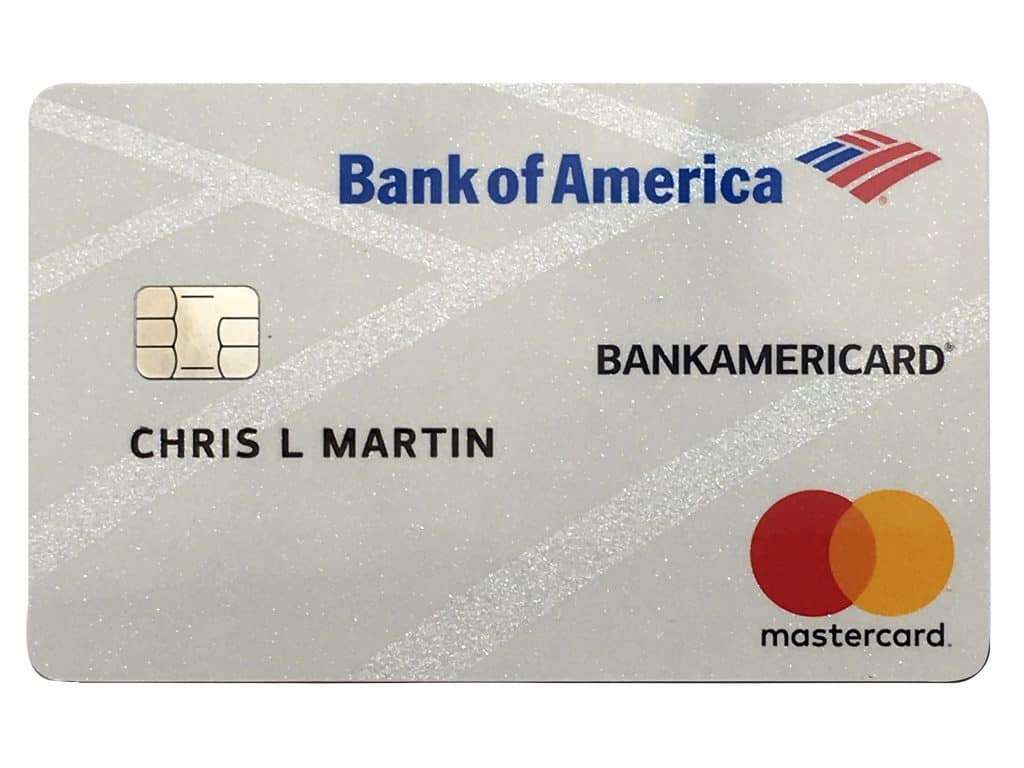

Bank of America’s BankAmericard is another popular low-interest credit card offering an extended 0% APR for 18 billing cycles. This introductory period applies for all purchases and bank transfers completed within the first 60 days of opening your account. A 3% fee is charged on bank transfers, but there are no annual costs or late APRs. The interest rates are also meager compared to other lenders — Bankamericard charges annual APRs of 15.24% to 25.24%. You can also access FICO scores via a web or mobile application.

Pros:

- Does not charge any annual fees

- Offers some of the lowest APRs in the market

- Includes a mobile application

- Has resources and excellent customer service

Cons:

- Limited 0% introductory APR on transfers

- Requires high credit score

This credit card uses a reward system that offers several benefits, including low overall APRs. They have a 12-month introductory period where you pay no interest on balance transfers after which a variable APR of 14.99% – 25.99% is charged. Blue cash preferred credit also offers various rewards including 6% cashback on supermarket purchases up to $6,000. If your annual supermarket purchases exceed this limit, you can still enjoy 1% cashback on all purchases. You also get 6% cash back on US streaming, 3% on transit and parking, 3% on US gas stations a credit statement worth $250 on your first $1,000 within three months of opening an account.

Pros:

- Very low APRs in the market

- Has several reward programs

- Card accepted in over 1.6 million places across the USA

- Ideal for balance transfers and office purchases

Cons:

- Charges an annual fee of $95

- Keen on credit scores

PenFed Promise Visa Card offers the lowest regular APRs in the market. Their rates vary from 11.99% to 17.99% depending on your credit score. You also get a $100 sign up bonus, and there are no annual fees charged. However, this card has no zero-interest introductory period. Instead, you are offered a reduced 4.99% APR for the first 12 months before regular rates resume. This APR is only charged on balance transfers. PenFed charges no cash advance fees, bank transaction fees, or late payment APRs. It is one of the few credit cards that pair low interest with a sign-up bonus. They also charge a low balance transfer rate.

Pros:

- Offers amazing sign-up bonus

- No annual fees required

- Very low-interest rates

- 0% cash advance rate

Cons:

- No introductory purchase APRs

- Charges a balance transfer rate

Lake Michigan Credit union offers one of the lowest ongoing rates in the market. Qualifying applicants can enjoy a low 8.5% APR on bank transfers. Although the lender only has offices in Michigan and Florida, anyone can join if they offer a minimum $5 donation to ALS charity. Prime Platinum credit card charges no annual fees. However, they charge 2% on foreign transactions. Regular APRs range from 8.5% to 18% depending on your creditworthiness. Other offers include car rental insurance, 24-hour member service, and emergency card replacement.

Pros:

- Easy to qualify for a card

- Very low ongoing APRs on transfers

- Complimentary car rental insurance

- No annual fees

Cons:

- No introductory APRs

- Charges 18% APR on balances later than 60 days

Chase Slate is another low-interest credit card that charges annual APRs from 17.24% to 25.99%. Besides offering low rates, slate does not charge any yearly fees. The card also comes with an 11-month 0% introductory rate on purchases and bank transfers. Cash advance is charged at 5% or $10 while the foreign transaction rate is 2%.

Pros:

- No annual fees

- Very low yearly rates

- No late fees and APRs

- Ideal for transferring large balances

Cons:

- Not available for members with promotional rate cards

- Shorter introductory period

How to obtain a low-interest credit card?

I. Negotiate a lower rate

The first and most recommended method for getting a small interest credit card is to negotiate with your current credit provider. Call and ask them whether you can get a lower rate on your credit card. Most lenders have set terms on how to inch closer to lower interest rates. It may include paying your balances on time, using your card more often or even being a loyal customer with the lender.

II. Transfer to credit with low interest

If you are currently paying more than you should, and there are better options, you can apply for a new credit card that has low interest. You can also transfer balances, although this may put you in an awkward position if the balance is significant to start with.

III. Work on your credit score

As with most line of credit products, interests tend to go higher when you have a poor track record with credit bureaus. Lenders consider those with bad/poor credit score to carry a higher risk of default. You should, therefore, work on developing a creditworthy history. There are various ways to do this, but it mainly involves borrowing and paying back on time. With a high score, you can easily qualify for low-interest credit cards

Bottom line

There are several other low-interest credit cards available for eligible candidates. When looking for a low-interest credit card, it is recommendable to compare as many options as possible. This will help you identify offers with the best rates and terms. Having the lowest APR does not necessarily mean the offer is better. It may be tied with annual fees and transfer rates that make up for the low-interest rate charged. You should, therefore, look at all the critical aspects before choosing your card.

FAQs

What is the lowest interest credit card?

How is interest charged on my credit card?

Can I avoid paying interest?

Can my bank give me a lower interest rate?

What happens if I pay the bare minimum?

What is an APR, and how does it work?

What is a late payment fee?

Are interest rates charged monthly or annually?

Can I pay the balance before the bill?