What are the 10 Best Credit Cards in 2021?

Credit cards are very convenient and secure compared to debit card. Besides allowing you to stretch funds when your finances are tight, credit cards protect you from frauds and unauthorized users. Most credit card issuers offer protection covers for unauthorized purchases, faulty purchases and charge-backs.

You can also use credit cards to build your score with each payment you make on time. What’s more, credit cards eliminate the need to carry cash when traveling. You can use credit cards to keep track of your personal or business expenses.

Some lenders offer reward programs. If you like to travel a lot, for instance, having a credit card that allows you to earn redeemable miles is quite attractive. Besides offering the essential services of a credit card, this option saves or earns you discount on an expenditure that you have more often. Nonetheless, credit cards come with varying interests, APRs, charges, and policies and there is no one-fit-for-all. As such, the best credit card is that which meets your current needs and situation.

Besides covering the best credit card providers, you will also get to understand why you need a credit card, how to qualify for one, as well as, some pros and cons of having a credit card.

Types of credit cards

These are standard credit cards issued on a revolving credit account, which means you can carry balances from one month to another. The balance difference must be paid in full at the end of each month to avoid interest. Cash-back credit cards allow you to earn some money back on your purchases. The issuer usually sets a limit and percentage you can earn back.

These are standard credit cards issued on a revolving credit account, which means you can carry balances from one month to another. The balance difference must be paid in full at the end of each month to avoid interest. Cash-back credit cards allow you to earn some money back on your purchases. The issuer usually sets a limit and percentage you can earn back.

These work like cash-back cards, only that instead of earning cash, the issuer offers redeemable rewards points. Rewards credit cards are popular among retail stores and supermarkets. Rewards may vary from points to air travel mileage, hotel accommodation and free services.

These work like cash-back cards, only that instead of earning cash, the issuer offers redeemable rewards points. Rewards credit cards are popular among retail stores and supermarkets. Rewards may vary from points to air travel mileage, hotel accommodation and free services.

Most credit cards are unsecured meaning the bank does not require cash deposit or collateral. Secured credit cards, on the other hand, work like debit cards. You need to deposit as much cash as you would want to spend on your credit card. These cards are ideal if you want to build history and credit score.

Most credit cards are unsecured meaning the bank does not require cash deposit or collateral. Secured credit cards, on the other hand, work like debit cards. You need to deposit as much cash as you would want to spend on your credit card. These cards are ideal if you want to build history and credit score.

These credit cards allow you to transfer balance owed in one card to another card. Balance transfer credit cards are ideal f you are looking for a low-interest card to replace your current choice. They come with lengthy interest-free periods (up to 12 months) allowing you to manage your balances with less effort.

These credit cards allow you to transfer balance owed in one card to another card. Balance transfer credit cards are ideal f you are looking for a low-interest card to replace your current choice. They come with lengthy interest-free periods (up to 12 months) allowing you to manage your balances with less effort.

There are several other minor categories of credit cards in the market. These include retail credit cards that are issued by a store. You can only use them in the specific store. Gas credit cards are more like retail cards, albeit used in gas stations. Platinum and gold credit cards are offered to members with excellent credit score. Other variations include low-interest credit cards and corporate credit cards.

There are several other minor categories of credit cards in the market. These include retail credit cards that are issued by a store. You can only use them in the specific store. Gas credit cards are more like retail cards, albeit used in gas stations. Platinum and gold credit cards are offered to members with excellent credit score. Other variations include low-interest credit cards and corporate credit cards.

What you should consider when finding the best credit card?

i. Interest rates and card policies

Banks and lenders that offer credit cards operate within set market regulations. However, they still have varying policies regarding their products, services, features, charges, and offers. Credit card interest rates vary significantly from one lender to another. Comparing the best credit card rates is one way of finding the lowest prices in the market. It is also crucial to read through the policies and determine whether you have the discipline to follow through with the terms. Some cards are safer and more affordable than others.

ii. Look for a card that is suitable for your needs

As aforementioned, credit cards come in various types designed for specific requirements. If you have a bad credit score, it will be challenging to qualify for cards that require great to excellent ratings. If you own a distribution company, on the other hand, having a credit card that offers redeemable points for gas seems like a feasible option. It is, therefore, essential to understand your needs and personal circumstances. With this in mind, you can set out to find the best card for your unique needs.

iii. Improved customer features

Excellent credit cards offer something more than low rates and APRs or redeemable reward points and cashback. They provide new features that make shopping and managing your balances much easier. It could be an online calculator, pre-qualification, mobile app or notification service, a waiver on late fees or $0 charge on foreign transfers; the list is probably longer. If you seek these features, then you must compare your options and find a card that has them.

iv. Better customer service and convenience

Besides low rates and suitable terms, the best cards are associated with exceptional customer service. Some lenders allow you to finish the online application and mail the credit card. They also provide online customer support, account management, and resourceful tools. Others have better frameworks and reach, so it is much easier to use their credit cards. The best credit cards should be affordable and convenient to use.

The Pros

- Less stringent terms

- Lower rates and APRs

- Usable in many places

- Great for building a credit score

- Rewards and cashback

The Cons

- Encourages overspending and recurrent debt cycle

- Misuse ruins your credit score and access to future loans

- Credit cards are synonymous with expensive fees and interests

Criteria used to rank the best credit cards

- Monthly interest rates and APRs

- Types of credit cards offered

- Minimum qualification requirements

- Terms, fees, and charges

- Availability of reward programs and bonuses

- Market availability (local branches)

Top 10 best credit cards

Chase Freedom Unlimited is one of the leading credit cards in the market. It offers an exciting rewards program that allows holders to earn flat percentage cash back on their purchases. You automatically earn 3% cashback if you spend a minimum of $20,000 within the first year of opening an account. After the year, regular cashback is 1.5% on all purchases you make. The credit card charges $0 annual fees and has a 15-month no zero-interest introductory period. Normal APRs start from 17.24% to 25.99%. Chase Freedom Unlimited is ideal if you have a good credit score and need low-interest credit cards with a reward program. The card as well allows for the transfer of balances from other banks.

Pros:

- Charges very low-interest rates

- Has one of the best reward programs

- No annual fees

- Exposes one to lengthy 0% introductory APR

Cons:

- Strict qualifications

- Charges balance transfer fees

American Express Blue Cash Preferred Credit card is another great offer if you are looking to earn more of your money back. This credit card is offered with a 25% cashback on your first $1000 spent within three months of opening an account. You instantly earn $250 back. The card has a lot of offers including 6% cashback on all supermarket purchases under $6,000 per year, 3% of gas station purchases, 6% of select streaming and TV, 3% on ground transport and 1% on all other purchases. You can also earn $360 if you can max out the grocery rewards. Blue Cash Preferred has a 12-month 0% introductory APR on purchases and bank transfers. After the twelve months elapse standard APRs resume at 14.99% – 25.99%. The rate will depend on your creditworthiness. Blue Cash also charges an annual fee of $95.

Pros:

- The credit card has some of the lowest APRs and interests

- The card comes with rewarding cashback program

- Usable in over 16 million places in the US

- Great for daily home or office purchases

Cons:

- Requires great to excellent credit score

- Charges an annual fee of $95

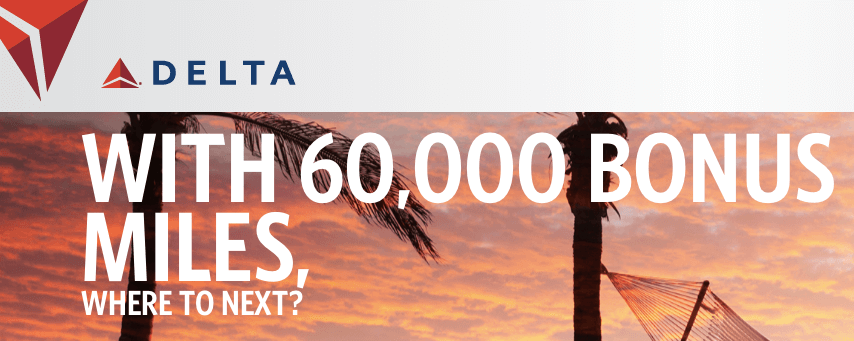

Gold Delta Sky-Miles is ideal if you are looking for an airline credit card. This card comes with several amazing features and rewards. You can earn 30,000 miles on the first $1,000 you spend on whatever purchases. You also earn 50% cashback on all purchases made within the first three months. Once the introductory period is over, you will start earning 2 miles per dollar spent on Delta and 1 mile per dollar spent on other purchases. This card charges no fee for balance transfers and waivers the first year’s annual fee of $95. It also waivers the fees for the first checked bag and gives you access to Cabin-1 boarding. Normal APRs stand at 17.74% – 26.74%. Gold Delta Sky-Miles is ideal if you love to travel, with miles redeemable at any time with no expiry.

Pros:

- No foreign transaction fees

- Very low APRs and rates

- Attractive cashback program

- Suitable for travelers

Cons:

- Charges a $95 annual fee

- 50% cashback is limited up to $300 only

The Chase Ink Business Preferred credit card is designed as a credit card for business people who travel a lot. The card does not charge anything for foreign transfers. However, you will be charged an annual fee of $95, with APRs varying between 18.24% and 23.24% depending on your creditworthiness. This credit card allows you to earn 800,000 points on your first $5,000 purchases within three months of opening an account. You also earn 3 points per dollar on your first $150,000 purchases and 1 point per dollar once you pass that threshold. You can redeem your bonus points through the Chase Ultimate Rewards portal to enjoy 25% more value on your points. Points are redeemed for airfare, cruises, car rentals and hotels, shipping, cable, internet, phone, and advertising, among others. You can also transfer your points to a partner reward program.

Pros:

- Highly rewarding points

- Points are transferable on a 1:1 ratio

- Has low APRs

- A convenient way to redeem points

- Usable in several categories

Cons:

- Charges an annual fee

- No 0% introductory APR

Wells Fargo Cash Wire credit card is one of the best products offered by the lender. Like most Wells Fargo cards, Cash Wise charges a very low-interest and has an extended 18-month 0% introductory APR. You get additional cell phone protection covers against unauthorized use. Cash Wise also allows you to earn $150 if you spend up to $500 within the first three months. All other purchases have a flat reward rate of 1.5%. Digital wallet purchases like Google Pay and Apple Pay earn you 1.8% cash back for the first twelve months after you open an account. The rewards are redeemable at any Wells Fargo ATM. Other features include 0$ annual fees, free foreign transfers, and free digital tools.

Pros:

- You can get cash advance

- Cell phone protection cover of up to $600

- Charges $0 annual fees and foreign transfers

- Very low-interest rates

Cons:

- Charges a fee for late repayment

- Keen on credit scores

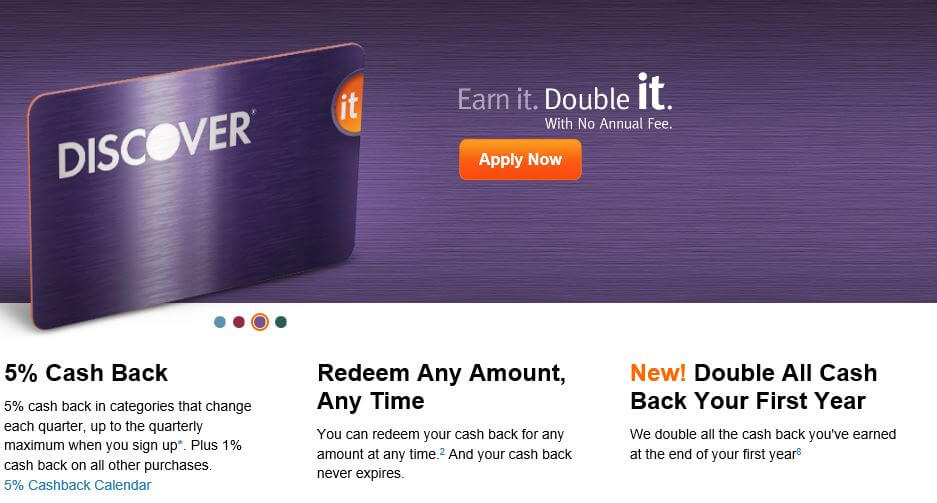

Cash Back credit card is one of the most affordable options in the market. With low APRs ranging from from14.24% to 25.24% and extended 14-month zero interest duration, this credit card allows you to maximize cashback during the first year. The card has a 5% reward rate on all purchases that reach $1,500 quarterly. You also earn 1% for purchases that exceed this cap. Within the first year, Cash Back matches your rewards. This means you can enjoy a 10% reward rate on purchases up to $1,500 (quarterly) and 2% on other purchases. You also earn $75 if you max your rewards. If maxed in the first year, the amount is matched to $150 in total. Rewards can be redeemed in restaurants, gas stations, Amazon.com, and select gas stations. Discover it Cash Back credit card charges no annual fees

Pros:

- Rewards highly for the first one year

- Offers free notification if your details appear in dark web

- Redeem rewards at any time – no expiry dates

- Low-interest rates

Cons:

- 0% introductory APR is only available for balance transfers

- High credit card score qualification

HSBC Cash Rewards MasterCard gives you the chance to earn part of your cashback through a rewarding bonus program. The card offers a 3% cashback on all purchases up to $10,000 during the first year. You also get a 1.5% cash back on other purchases that exceed the limit. No annual fee is charged. Normal APRs start at 13.24% to 17.24% depending on your score. You need a good to excellent score to qualify for the HSBC Cash Rewards credit card. You also get a 10% universal bonus on all the rewards you have earned throughout the year. HSBC offers cash advance and $0 foreign transfers.

Pros:

- Significantly lower interest rates

- One year waiver on late payment

- $0 annual fees and foreign transaction fees

- Extended introductory period (18 months)

Cons:

- High eligibility requirements

USAA offers one of the lowest interest rates of any credit card you will come around. Starting at only 9.15%, Rate Advantage Visa Platinum credit card has the best offer for qualifying members. It comes with a six-month introductory period where you are charged 0% interest on purchases and balance transfers. Once the period elapses, the normal APRs range from 9.15% to 26. 15%. However, you must be an active or retired member of the military or family member of the same to qualify for USAA Rate Advantage. If you are on an active mission, the APR drops to 4% until your task is over. Station leaders also enjoy a 4% APR for twelve months during dispatch. No annual fee is required. However, you will be charged up to 3% for a cash advance and balance transfers.

Pros:

- Lowest APRs in the market

- easy and convenient to use

- Charges $0 annual fees

- Easy qualification if you are in the military

Cons:

- Charges balance transfers and cash advance

- limited to military customers

This is another exceptional credit card for those who seek low interests paired with high rewards. The card carries 0% introductory APR that lasts the first 18 billing cycles following your account opening. This makes it ideal for transferring large balances. No annual fees are required. US Bank Platinum also offers cell phone production up to $1,200 per year if you use your card to pay for cell phone bills. Normal APRs of 14.49% to 25.49% resume once the introductory period is over. As a Visa, US Bank Platinum credit card is usable in various places. It is one of the traditional credit cards that are easy to understand and convenient to use. There are very few features and straightforward terms.

Pros:

- Low annual percentage rate

- Extended 0% introductory APR

- Cell phone protection

- Available in all the 50 states

Cons:

- No reward points, cash back or bonuses

- Keen o credit score

When most credit companies target customers with excellent credit score, OpenSky Secured Visa offers something for those with a less than average credit score – credit card for bad credit. It does not rely on credit score alone. This card is perfect if you have had delinquencies or bankruptcy. OpenSky Secured offers a variable APR around 19.64% and charges an annual fee of $35. As a secured card, you need to make a security deposit of $200 – $3,000, which acts as your security. This card also helps build your credit history and reports are sent to all the three major credit bureaus. However, you may not be able to convert your card to unsecured unless you apply for a card with another issuer.

Pros:

- Accepts debit cards, wire transfers, physical check or money order and Western Union

- Quick approval time

- Builds your credit score

Cons:

- Requires a deposit for security

- Charges annual fees

How to get the best credit card

I. Improve your score

If you want to qualify for the best credit cards, you need a high to excellent credit score, to begin with. There is the best option for every set of needs. However, some cards have low-interest rates, less-stringent policies, and massive bonuses. Most lenders that offer these cards also have higher qualifications. An excellent score reduces your risk and improves your creditworthiness among lenders. Increase your score by paying your loans and dues on time, and you will soon be qualifying for the best credit cards in the market.

II. Assess your needs

To get the best card, you must know your needs. A card that is great for one person may have nothing much for another. Once you know what you need and how you will use the card, it becomes much easier to find the right product. You should also read the terms and make sure you can meet all of them. If they are too strict, you can always find better options for your needs.

III. Compare various offers

The only way you can get the best credit card is through comparison. Best is by itself, a comparative that requires more than one product. The more credit cards you review, the more knowledge you will have about what they offer and if the terms suit your needs. In other words, you will be narrowing the search to best credit cards for your unique needs.

Bottom line

The several types of credit cards that exist in the market are enough reason to step back and review your options before making a decision. No single credit card is one-fit for all. Your circumstances and finances determine the range of choices you have. As a customer, you should review existing offers and find those that best align with your needs. Before applying for a credit card, make sure you understand how it works, how much you can borrow, interest rates, deadlines, and late fees and transaction processing, among other things. This way, you will be able to get a credit card that is easy to manage and does not get you into more debt than necessary.

FAQs

What are the different types of credit cards?

How do Visa cards differ from MasterCard?

Do I qualify for a credit card?

How much longer until my credit card arrives?

How much do I pay for a credit card?

What rates are charged on my credit card?