Bond Yields: What are Bond Yields and Why do They Matter?

Bond yields dictate how much interest you should be paid for making an investment. They matter for two key reasons. Firstly, the original yield attached to bonds when they were first issued – known as coupon payments, is the fixed amount of interest that you will receive every 6 or 12 months.

Secondary, the yield on bonds will go up and down on the secondary markets. So, if you plan to invest after the bonds were issued, or sell them before they mature, the yield will impact the real-world value of the bonds.

In this article, we explain the ins and outs of what bond yields are, how they work, and why they can impact the value of your investment.

-

-

Featured Bonds Broker 2020

- Minimum deposit and investment just $5

- Access to Bonds, as well as Stocks and Funds

- Very user friendly platform

What are Bond Yields?

Whether its traditional stocks and shares, ETFs, or mutual funds, all investments will come with a yield. In its most basic form, the yield refers to the amount of interest that you make on your money. For example, if you invest $10,000 and the yield is 5%, you would make $500 on your investment.

Whether its traditional stocks and shares, ETFs, or mutual funds, all investments will come with a yield. In its most basic form, the yield refers to the amount of interest that you make on your money. For example, if you invest $10,000 and the yield is 5%, you would make $500 on your investment. The yield on bonds is somewhat different from other financial instruments. This is because you will have both a ‘fixed yield’ and a ‘variable yield’ that changes depending on market forces – more on this later. So, when a company or government issues new bonds, they will determine the amount of interest that they wish to pay to bondholders.

The specific rate will depend on a range of factors, such as the health of the company’s balance sheet for corporate bonds or the state of the economy for government bonds. This is all related to the risk of the bond as an investment. For example, if the US government were to issue new bonds, the yield would be very low.

This is because the risks of default are virtually non-existent, not least because the US government could simply print more money via the Federal Reserve. At the other end of the spectrum, corporate bonds issued by a company that has been struggling in the stock markets would come with more attractive yield, as the risks of default are much higher.

Fixed Bond Yields – Coupon Rate

The original yield paid on bonds is known as the ‘coupon rate’. Expressed as a percentage, the coupon rate will never change. For example, let’s say that you purchased bonds from Apple PLC at a coupon rate of 2%. You would be paid $20 annually for every $1,000 bond you held until the bonds mature. This yield would never change as long as you don’t sell the bonds on the secondary market.

The original yield paid on bonds is known as the ‘coupon rate’. Expressed as a percentage, the coupon rate will never change. For example, let’s say that you purchased bonds from Apple PLC at a coupon rate of 2%. You would be paid $20 annually for every $1,000 bond you held until the bonds mature. This yield would never change as long as you don’t sell the bonds on the secondary market.This is ideal for those of you that wish to benefit from passive income. In other words, once you purchase the bonds in question, you won’t need to do anything until they mature. Throughout the course of the term, you will receive the same amount of fixed coupon payments, which is usually every 6 or 12 months.

For example:

- Nike PLC issues $100 million worth of corporate bonds at a yield of 6%

- Nike PLC issued the bonds at a maturity of 7 years and the coupon payments are distributed annually

- Each bond is worth $500, so you decide to buy 20 totaling $10,000

- At the end of year one, you would receive a coupon payment of $600 ($10,000 x 6%)

- You get a further $600 every year until the bonds mature

- 7 years later, you then receive your original $10,000 back

- Over the course of the term, you would have made $4,200 profit on your investment ($600 x 7 years)

The overarching concept is that you do not need to worry about the yield on the bonds once you buy them if you have no intention of selling them before maturity. As we cover in the next section, you only need to have an understanding of the running bond yield if you want to offload your bonds early.

Running Bond Yields

As soon as bonds are issued by companies or governments, the yield is likely to go up or down in the open marketplace. This will have a direct correlation to the financial health of the issuer or the specific sector, market, or economy that the issuer operates in. The easiest way to get your head around the ‘running yield’ is to think about traditional stocks and shares.

- For example, let’s say that you hold shares in British American Tobacco.

- If the European Union decided to increase the tax on tobacco companies operating within the European block, this would have a direct impact on profits, so the share price of British American Tobacco would likely go down.

- This means the risks of the investment go up.

So, in the case of bonds, the value of the bonds will also go up and down depending on market conditions. For example, let’s say that you purchased Treasury bonds from the US government. If the US economy grew by a smaller percentage than the markets had hoped for, the value of the bonds would go down. What happens when the value of bonds go down? The yield goes up.

This is super-confusing for newbie-investors to understand at first glance, so let’s look at a couple of examples.

Example 1: Bond Yield Goes UP

Let’s say that Ford Motors issues bonds at an original yield (coupon rate) of 4%. This means that for every $100 bond, you would make $4 interest per year.

- Two years after the bonds are issued, Ford Motors runs into financial difficulties

- This means that the risks of the bonds are higher

- If you then attempted to sell the bonds on the secondary market, those buying the bonds would want to be paid a higher rate of return to compensate for the higher risk levels

- As such, your 4% yield is no longer attractive to new investors

- Instead, investors want to be paid a yield of 6%

- In order to meet the demands of the market, you would need to sell the bonds at a discount

- This is because the 4% coupon rate on the bonds is fixed, so you’d need to sell the bonds for less than you originally paid

Example 2: Bond Yield Goes DOWN

Let’s stick with the same metrics as the example above, so we’ll base our calculations on bonds issued by Ford Motors at an original yield (coupon rate) of 4%.

- One year after the bonds are issued, Ford Motors surpasses market expectations and its shares are sky-rocketing on the NYSE

- This means that the risks of the bonds are much lower

- If you then decided to sell the bonds on the secondary market, you would want to be paid more than you originally paid for the bonds

- As such, investors would expect a lower yield than the 4% coupon rate

- In order to meet the demands of the market, you would be able to sell the bonds at a premium

- This is because the 4% coupon rate on the bonds is fixed, so you’d be able to sell them for more than you originally paid

As you can see from the above, as the bond yield increases, the risk goes up. This means that bondholders need to sell their bonds at a discount. At the other end of the spectrum, as the bond yield decreases, the risks go down. As such, bondholders can sell the bonds at a premium.

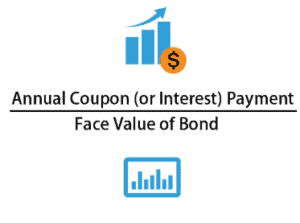

Calculating Bond Yields

When it comes to calculating the yield on bonds you purchased at the time of issue, you simply need to look at the size of the coupon payments you receive in relation to the bond value. For example, if each bond has a value of $500 and you receive $50 per year in coupon payments, then the yield is 10% ($500 / $50).

However, calculating the running yield on bonds is not as easy, as you need to factor in the premium or discount that the bonds were bought or sold at.

- To keep things simple, let’s say that Tesla originally issued bonds at a yield of 5%, with each bond worth $500

- This means that the bonds pay $25 per year in coupon payments ($500 x 5%)

- With Tesla growing at an exponential rate, the bonds are now selling at a premium

- Those holding the bonds no longer want to sell them at their face value of $500

- Instead, bondholders are asking for $750 per bond

- This means that you are paying a 50% premium on the bonds ($500/$750)

Sticking with the same example as above, the 50% premium that you paid on the bonds needs to represented as a running yield. As the coupon rate pays 5%, and you paid 50% higher than the face value, we then need to recalculate the value of your investment.

- You purchased Tesla bonds at a 50% premium

- Each bond still has a face value of $500 even though you paid $750

- So, you will still receive $25 per year, per bond, in coupon payments ($500 x 5%)

- As such, for every $750 that you paid for the bond, you would receive $25

- We then need to divide the $25 coupon payment into your $750 investment to get a new running yield

- This amounts to a bond yield of 3.33%.

As you can see from the above example, the running bond yield went from an original rate of 5% down to 3.33% as the value of Tesla increased. This is because bondholders sold the bonds at a premium. If Tesla was to lose value in the open market, the above example would remain the same but in reverse. For example, you would be able to buy the bonds at a discount, meaning your running yield would be higher than the original coupon rate of 5%.

Negative Bond Yields

A rather strange phenomenon made its way to the multi-trillion-dollar bond space recently; negative bond yields. In order to set the scene, let’s remember that the overarching purpose of investing in the financial markets is to make money. After all, this is why you are risking your hard-earned cash. If you were to make an investment without expecting a return, the process would be financially counter-intuitive!

A rather strange phenomenon made its way to the multi-trillion-dollar bond space recently; negative bond yields. In order to set the scene, let’s remember that the overarching purpose of investing in the financial markets is to make money. After all, this is why you are risking your hard-earned cash. If you were to make an investment without expecting a return, the process would be financially counter-intuitive!This is why the yield on bonds has always been, until recently, positive. However, with countries around the world still unable to regain pre-2008 GDP growth levels, central banks have been cutting interest rates as never seen before. As interest rates can only go so low, a number of central banks have since toyed with the idea of negative interest rates. This means that the yield on the government-issued bond is negative, so you actually make a loss by investing your money.

We’re not just talking about emerging economies here, there are now heaps of first-world nations that have decided to cut interest rates on bonds to negative territory. This includes:

- Japan -0.10%

- Germany -0.84%

- France -0.24%

- Netherlands -0.64%

- Sweden -0.52%

- Switzerland -0.92%

- Belgium -0.32%

It is important to note that negative yields are set by the central bank that issues them, and not the markets. If you’re wondering why this is, the concept of issuing negative yield bonds is to boost the underlying economy. Effectively, it’s to prevent large institutions from hoarding money in savings accounts, and instead, lend it out to everyday consumers.

It’s often difficult to get your head around bonds that come with a negative yield, so let’s look at a quick example.

- You purchase $10,000 worth of bonds at a yield of -1%

- The bonds have a maturity of 10 years

- While you would normally get a coupon payment at the end of each year for loaning your money to the bond issuer, negative yields pay nothing

- Instead, YOU are effectively paying the issuer annual coupon payments for holding the bonds!

- As such, when the bonds eventually mature in 10 years time, you will get less than you originally paid

You might be surprised to learn that negative yield bonds have been flying off the shelf in recent years. This is because investors would rather pay a premium to guarantee the safety of their money through low-risk government securities, as opposed to being exposed to a stock market crash.

What Bond Yields Should I aim for?

Regardless of the type of asset you are investing in, the yield that you aim for will need to reflect your personal appetite for risk. As we have noted throughout our guide, as the risk of the bonds goes up, as should the yield.

Below we have listed some examples of the types of bond yields currently available in the market. We’ve included a mixture of corporate bonds and government bonds and showed you an example of how much money you would make on a $10,000 investment.

Corporate Bonds

Nike PLC – 2.06% Yield – Mature in 2026

If you’re looking for some high-grade, low-risk corporate bonds, Nike PLC might be worth considering. The coupon rate pays 2.3750%, and the bonds mature at the tail-end of 2026. However, Nike PLC bonds are now selling at a premium, so your running yield is reduced to just 2.06%.

- Invest $10,000

- 4 years worth of coupon payments

- Running yield of 2.06%

- Returns of $206 per year

- Total return on investment = $10,824

Western Union – 5.15% Yield – Mature 2036

If you’ve got a higher appetite for risk and you’re looking for a super-long-term investment, it might be worth exploring Western Union bonds. The bonds were originally paying 6.20%, although the current yield amounts to 5.15%. The bonds do not mature until 2036, so you’ve got the chance to earn 16 years worth of coupon payments.

- Invest $10,000

- 16 years worth of coupon payments

- Running yield of 5.15%

- Returns of $515 per year

- Total return on investment = $18,240

Government Bonds

US Treasury Bonds – 0.65% Yield – Mature 2030

At the time of writing this article, the economic impact of the 2020 Corovirus is clear to see. This is because, for the first time ever, US Treasury bond yields have dropped below 1% (unless investing in a 30-year security). As such, you’ll get just 0.65% on a 10-year Treasury bond, which is the price to pay to protect your wealth from an economic downfall.

- Invest $10,000

- 10 years worth of coupon payments

- Running yield of 0.65%

- Returns of $65 per year

- Total return on investment = $10,650

Does a $650 return on $10,000 over a 10-year period represent a good investment? Absolutely not, as it doesn’t even cover the impact of inflation. With that said, you would at the very least protect your money from a potential crash of the financial markets.

Turkey Government Bonds – 12.095% Yield – Mature 2030

If you’ve got a really high appetite for risk, and you’re prepared to lock your money away for 10 years, you might be tempted by the bond yields currently being offered by the central bank of Turkey. The government bonds are paying an annual yield of 12.095%, which is significantly higher than what you’ll get by investing in US Treasuries. On the flip side, the risks of a default are considerably higher, especially considering the current state of the Turkish economy.

- Invest $10,000

- 10 years worth of coupon payments

- Running yield of 12.095%

- Returns of $1,209.5 per year

- Total return on investment = $22,095

Conclusion

By reading our guide from start to finish, it is hoped that you now have a firm understanding of what bond yields are, how they work, and why they have a direct impact on the amount of money you can make from a bond investment. Put simply, if you purchase bonds at the time they are issued and hold on to them until they mature, the yield will never change.

However, if you plan to purchase bonds on the secondary market or you wish to offload a bond investment prior to maturity, you do need to understand how the running yield will affect you. Ultimately, you are best advised to diversify your investment as best as possible. You can do this by holding a basket that contains bonds of varying risk levels, across multiple markets, industries, and economies.

Featured Bonds Broker 2020

- Minimum deposit and investment just $5

- Access to Bonds, as well as Stocks and Funds

- Very user friendly platform

Glossary of Bonds Terms

Bond

BondA bond is when companies or goverments need to generate funds and when you invest you will receive you lump sump back with interest at the end of your agreement.

Treasury BondBonds issued by the United States Department of the Treasury to finance government spending.

Treasury NoteA Treasury Note are bonds issued by the United States Department of the Treasury and last up to 10 years.

Treasury SecurityTreasury securities are the bonds issued to investors by the U.S. government

Municipal BondsA Municipal Bond is usually issued by local Governments to finance public projects such as roads, schools, and airports. You will recieve you lump sum and interest back at the end of the term.

Corporate BondsA Corporate Bond is issued by businesses to raise funds for expansions or projects. You will recieve you lump sum and interest back at the end of the term.

Premium BondsA Bond that has no interest rate but your investments are entered into prize draws to win £25 to £1mil.

Savings BondUsually offered by Banks and Building Societies, Saving Bonds will last for a fixed term and earn interest. You are not able to access the money during the fixed term.

Fixed Rate BondsA Fixed Bond will start and end with same Interest Rate.

FAQs

What is the difference between the coupon rate and running yield?

The coupon rate refers to the fixed interest payments that the bond issuer pays. The running yield refers to the current market value of the bonds on the secondary market.

Why do I need to pay a premium on bonds?

If the risk of the bonds goes down, as will the yield. This means that you need to pay a premium for the bonds.

Why do I need to sell my bonds at a discount?

If the risk of the bonds goes up, and you wish to sell them before they mature, you will need to do so at a discount. This means you’ll get less than you originally paid.

What are negative bond yields?

If you hold bonds that pay a negative yield, this means that you will get less than you originally paid when the bonds eventually mature.

How do interest rates affect the bond yield?

Although not an exact science, if a central bank increases interest rates, it’s usually because the economy is performing well and if the reverse is performing badly. As such, the yield on the bonds will go down, as the risks are lower.

Are corporate bonds risk-free?

Unlike US Treasuries, corporate bonds are never risk-free. This is because struggling companies do not have the backing of the US Federal Reserve, so there is always the risk of default.

See Our Full Range Of Bonds Resources – Bonds A-Z

Edith Muthoni

Edith Muthoni

View all posts by Edith MuthoniEdith is an investment writer, trader, and personal finance coach specializing in investments advice around the fintech niche. Her fields of expertise include stocks, commodities, forex, indices, bonds, and cryptocurrency investments. She holds a Masters degree in Economics with years of experience as a banker-cum-investment analyst. She is currently the chief editor, learnbonds.com where she specializes in spotting investment opportunities in the emerging financial technology scene and coming up with practical strategies for their exploitation. She also helps her clients identify and take advantage of investment opportunities in the disruptive Fintech world.

WARNING: The content on this site should not be considered investment advice. Investing is speculative. When investing your capital is at risk. This site is not intended for use in jurisdictions in which the trading or investments described are prohibited and should only be used by such persons and in such ways as are legally permitted. Your investment may not qualify for investor protection in your country or state of residence, so please conduct your own due diligence. Contracts for Difference (“CFDs”) are leveraged products and carry a significant risk of loss to your capital. Please ensure you fully understand the risks and seek independent advice. This website is free for you to use but we may receive commission from the companies we feature on this site.

Copyright © 2025 | Learnbonds.com

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policyScroll Up

The original yield paid on

The original yield paid on  A rather strange phenomenon made its way to the multi-trillion-dollar bond space recently; negative bond yields. In order to set the scene, let’s remember that the overarching purpose of investing in the financial markets is to make money. After all, this is why you are risking your hard-earned cash. If you were to make an investment without expecting a return, the process would be financially counter-intuitive!

A rather strange phenomenon made its way to the multi-trillion-dollar bond space recently; negative bond yields. In order to set the scene, let’s remember that the overarching purpose of investing in the financial markets is to make money. After all, this is why you are risking your hard-earned cash. If you were to make an investment without expecting a return, the process would be financially counter-intuitive!